Compare Top Medicare Plans From Major Carriers

To compare Medicare plans available in your area, click Compare Plans or call 888-349-0361 to speak with a licensed insurance agent.

A popular type of health insurance coverage for age 65 and older, U.S. adults is Medicare Advantage, also known as Medicare Part C. However, choosing the right plan can be difficult—nationwide, insurance providers offered a total of 3,550 different Medicare Advantage plans in 2021 alone[1]. Finding the right insurance plan is also highly customized to the individual. You can you see a list of plans you’re eligible for, only by supplying your ZIP code and demographic information, and even then, you’re likely differentiating between the features of approximately 30 plans.

Seeking the assistance of an independent, agnostic health insurance agent is the best way to navigate this overwhelming task. But, you can also begin by honing on the health insurance companies that, generally, provide the best Medicare Advantage plans, based on elements such as provider network size, additional benefits and coverage.

The Forbes Health editorial team determined the best Medicare Advantage providers of 2022, analyzing U.S. insurance companies that offer nationwide plans by the number of states they provide coverage in, the variety of benefits they offer, how they were ranked by the Centers for Medicare and Medicaid Services (CMS), how they were ranked in terms of their financial health by agencies like A.M. Best, how agencies like J.D. Power ranked them in the manner of consumer feedback and more. Read on to find out which providers placed on our list.

| Provider | Forbes Health Ratings | Coverage area | Additional benefits | CMS rating | Learn More | ||

|---|---|---|---|---|---|---|---|

Humana |

5.0

|

Offers plans in all 50 states and Washington, D.C. | Dental, vision, hearing, lifestyle, transportation | 3.6 | Get A Quote | On Medicare Enrollment’s Website | |

Blue Cross Blue Shield |

5.0

|

Offers plans in 48 states | Dental, vision, hearing, lifestyle, transportation | 3.8 | Get A Quote | On Medicare Enrollment’s Website | |

Cigna |

4.5

|

Offers plans in 26 states and Washington, D.C. | Dental, vision, hearing, lifestyle, holistic, transportation | 3.8 | Get A Quote | On Medicare Enrollment’s Website | |

United Healthcare |

4.0

|

Offers plans in all 50 states | Dental, vision, hearing, lifestyle, transportation | 3.8 | Get A Quote | On CoverRight’s Website | |

Aetna |

3.5

|

Offers plans in 44 states | Dental, vision, hearing, lifestyle, transportation | 3.6 | Get A Quote | On Medicare Enrollment’s Website |

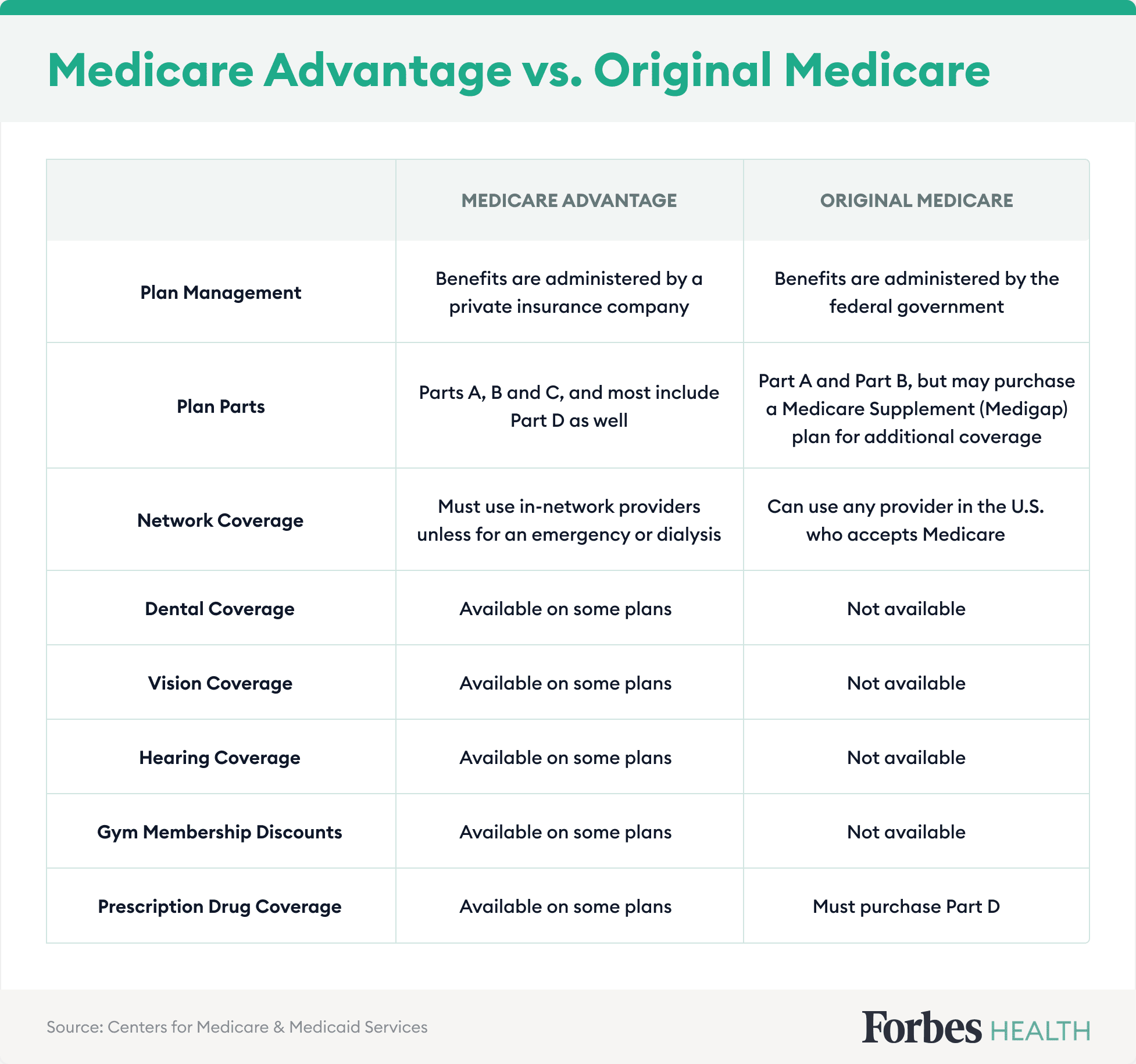

Medicare Advantage is an all-in-one plan choice alternative for receiving Medicare benefits. You may also hear it referred to as Medicare Part C. This plan is bundled with Medicare Part A and Part B and usually includes Part D, which provides prescription drug coverage. Medicare pays private insurance companies to administer the benefits of Medicare Advantage plans they sell.

Some Medicare Advantage plans offer valuable additional benefits, such as:

You can’t be enrolled in a Medicare Advantage plan and Original Medicare at the same time. To obtain Medicare benefits you’ve earned through payroll deductions before retirement, you must choose one of these plans.

During the open enrollment period, which runs from Oct.15 to Dec. 7 each year, you can join, switch or drop a plan for your coverage to begin on Jan. 1. If you’re already enrolled in a Medicare Advantage plan, you can switch to a different Medicare Advantage plan or Original Medicare during the Medicare Advantage open enrollment period, which starts on Jan. 1 and ends on March 31 annually. You can only make one switch during that time period.

If you’re already enrolled in Original Medicare (Parts A and B), you may be eligible to switch to a Medicare Advantage plan (Part C). You must be at least 65 years old or have certain disabilities, such as permanent kidney failure or amyotrophic lateral sclerosis (ALS). If the Medicare Advantage plan you choose doesn’t already have prescription drug coverage, you will have the option to enroll in Part D.

Some Medicare Advantage plans may have lower out-of-pocket costs than Original Medicare, and some have a $0 monthly premium. Here are a few questions to consider before purchasing a plan.

Once you’re enrolled in a Medicare Advantage plan, it becomes your primary insurance. The company handles paying all your claims. And every year, the cost of your plan will probably change. The plan provider (rather than Medicare) sets the amounts charged for premiums, deductibles and services. An Annual Notice of Change (ANOC) is mailed to you each September to be effective Jan. 1.

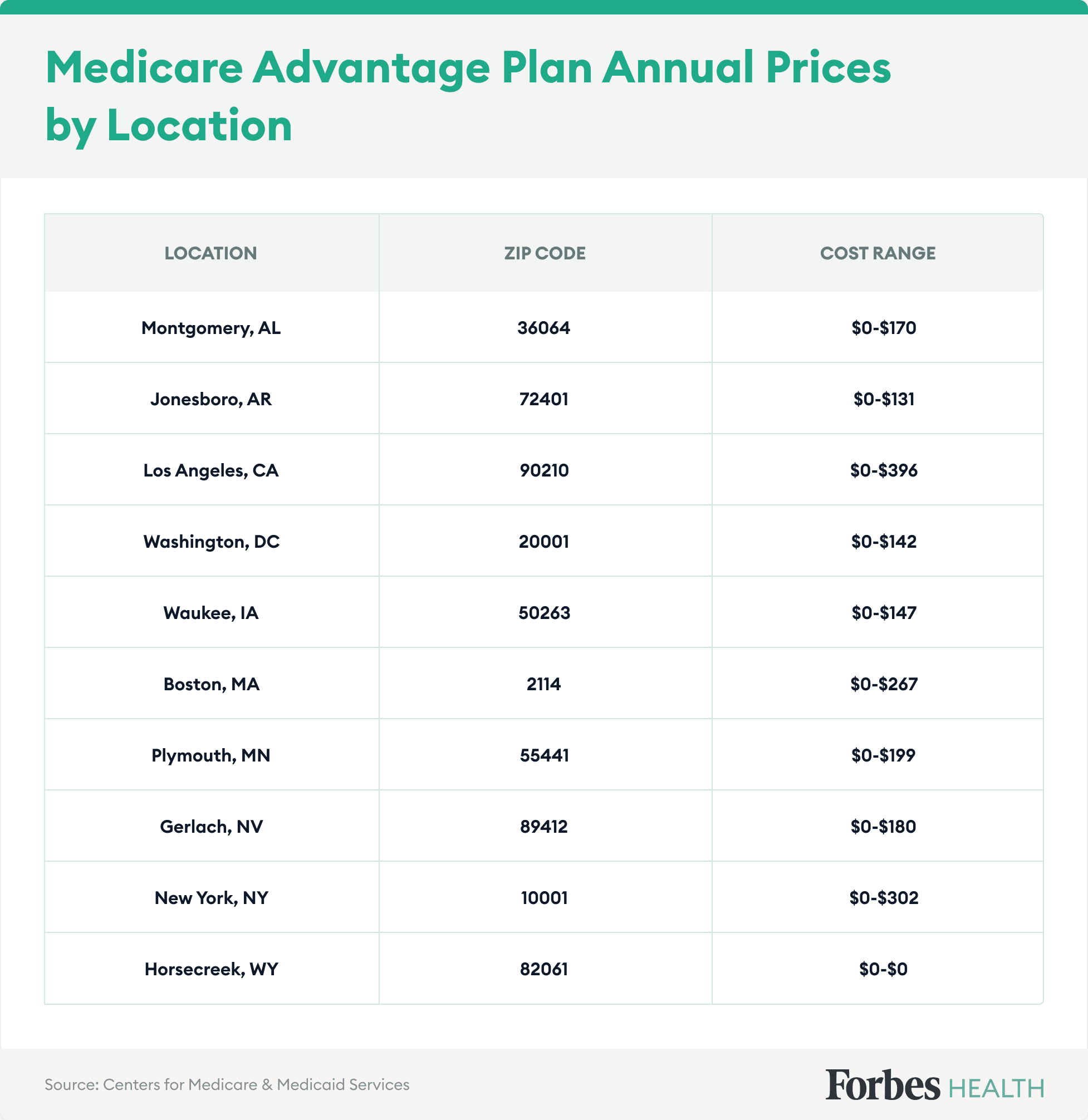

Factors like location play a major role in determining the cost of a Medicare Advantage plan. Costs are typically lower when you use providers in your plan’s network and service area. To find the specific cost of a Medicare Advantage plan in your zip code, visit Medicare.gov.

The following example shows how plan prices can vary significantly by location. Note: Your costs may differ from these ranges even if you live near but not in one of these areas, as rates are set by ZIP code.

Most Medicare drug plans have a coverage gap called the “donut hole,” which means there’s a temporary limit on what the drug plan will cover. “A person gets limited coverage while in the ‘donut hole.’ whether on a Medicare Advantage plan or a separate Part D plan,” says Antinea Martin-Alexander, founder of Advocate Insurance Group in South Carolina. “The individual will pay no more than 25% of the cost of the medication in the donut hole until a total out of $6,550 in out of pocket expenses is reached. There are different items that contribute to the out-of-pocket expenses while in the donut hole: any yearly drug deductible you may have, copays for any and all your medications, what the manufacturer’s discount is on that medication and what the insurance company pays for that medication,” she says.

There are four common types of Medicare Advantage plans to compare when making your selection.

Health Maintenance Organization (HMO)

Preferred Provider Organization (PPO)

Private Fee-for-Service (PFFS)

Special Needs Plans (SNP)

It’s easy to switch Medicare Advantage plans if you’re already using a Medicare Advantage plan. Enroll in a new plan during one of the open enrollment periods, and your old plan will disenroll you once your new coverage begins. If you receive medical insurance through an employer or elsewhere, speak with your provider to understand how you and your family’s coverage may change while under Medicare Advantage before deciding to make the switch.

“Find a knowledgeable insurance agent,” says Joe Valenzuela, co-owner of Vista Mutual Insurance Services in the San Francisco Bay area. “Having an agent doesn’t cost the member anything. Medicare insurance agents are subject matter experts—many have spent years learning the ins and outs of each plan they represent. There are also many nuanced differences between Medicare Advantage plans. An agent can narrow down the search to only those plans that most closely align with the client’s needs.”

Valenzuela recommends asking what is most important to you when choosing a Medicare Advantage plan and keeping that priority top of mind. He also suggests paying attention to the fine print in the plan you select.

“Once you narrow your search down to one or two plans, ook through the plan’s benefits line by line—you don’t want any surprises,” he says. “For example, a plan may have a low premium and copayments but might cost you much more each month in prescription copays.”

“A couple of important benefits to look at are the plan’s annual out-of-pocket maximum (the maximum amount the member could be responsible for in a calendar year) and your prescription drug costs,” adds Valenzuela. “Check all your medications on the plan’s formulary so you’re aware of the prescription copayments, deductibles and any restrictions.”

Consider the following details when deciding whether a Medicare Advantage plan or Original Medicare is best for you.

Medicare Advantage plans have some elements you might find appealing, as well as other features that may not match your needs. Consider both the benefits and drawbacks below before enrolling in a Medicare Advantage plan.

Medicare Advantage Benefits

Medicare Advantage Drawbacks

To determine the best Medicare Advantage providers of 2022, the Forbes Health editorial team evaluated all insurance companies that offer plans nationwide in terms of:

We focused exclusively on providing general summaries of the companies and their reputations. In order to provide specific plan recommendations accurately, it’s important to take into account the ZIP code and demographic details of the individual seeking insurance coverage. To do so, we recommend using Medicare.gov’s plan finder tool or seeking the expertise of an independent, agnostic insurance agent.

Ready To Find A Personalized Medicare Plan?

Keep your doctors, maximize your benefits, and save money when you use CoverRight’s online platform to compare Medicare Plans.

Information provided on Forbes Health is for educational purposes only. Your health and wellness is unique to you, and the products and services we review may not be right for your circumstances. We do not offer individual medical advice, diagnosis or treatment plans. For personal advice, please consult with a medical professional.

Forbes Health adheres to strict editorial integrity standards. To the best of our knowledge, all content is accurate as of the date posted, though offers contained herein may no longer be available. The opinions expressed are the author’s alone and have not been provided, approved or otherwise endorsed by our advertisers.